When will interest rates fall, and what will this mean for commercial lending?

Keeping abreast of key economic data and trends can be important for those involved in the UK real estate sector.

So, take a look at the latest report from the chief analyst at Kvika Securities, who provide us regular economic bulletins.

We hope you find this useful.

Interest rates remained unchanged in March

The most recent analysis was put together at the same time the Bank of England (BoE) Monetary Policy Committee (MPC) was making its monthly interest rate decision.

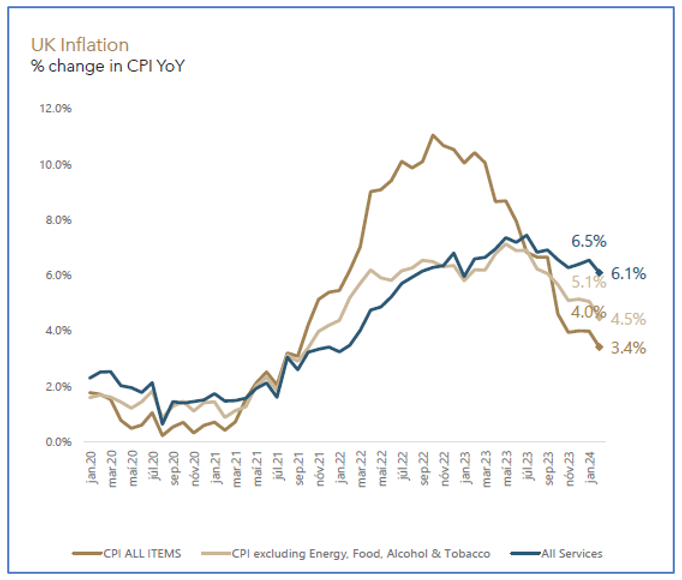

A lower-than-expected Consumer Prices Index (CPI) inflation rate announcement of 3.4% in the 12 months to February prompted some of the more bullish analysts to predict an immediate base rate cut of 0.25%.

This belief was reinforced by other positive indicators, such as the core rate of inflation falling from 5.1% to 4.5%, and services inflation easing from 6.4% to 6.1%.

Similarly, private sector wage growth – another key measure – provided more positive news as it is on track to come in at 5.4% in the first quarter of 2024, below the MPC projection of 5.7%.

Source: Kvika Securities

However, what we got was a “steady as she goes” confirmation that the base rate will remain unchanged at 5.25%.

One positive sign was that, unlike last month, none of the nine MPC members were in favour of a rate hike, with a near-unanimous 8-1 vote in favour of no change at the present time.

There are clear signs that the Bank of England medicine is working

It’s clear that the restrictive policy being followed by the BoE is working and helping to drive inflation down, a prerequisite for a rate cut.

However, the stubbornly high rates of wage growth and service inflation still point to sticky price pressures, which prompted the restrictive stance adopted by the MPC that it feels is required until persistence dissipates.

Encouragingly, for the first time, the MPC was able to explicitly confirm the possibility of reducing interest rates while at the same time maintaining its restrictive stance.

The major sticking point would appear to be wage growth, still running above 6%. There are suggestions that it needs to be trending between 3-4% before the MPC will rest easily.

Suggestions are that we should expect a rate cut in June

Our economic analysts are still predicting that there will be a rate cut in June, which is a view shared by many.

The expectation is that by then, the MPC should have two months of data showing inflation at or below target as well as softening core, service, and wage growth figures. These could prompt a cautious first cut with a cautionary hawkish messaging.

Source: Kvika Securities

However, one word of caution is that the US Federal Reserve (Fed) is not expected to cut its base rate until July, as US inflation is taking longer to come down than previously anticipated. This would mean the MPC taking the rare step of cutting interest rates before the US does.

Against that, though, is the fact that US rate cuts will be a celebration of inflation being tamed, rather than any equivalent UK cut that will be driven more by economic weakness.

Indeed, the New York Times reported the Fed suggesting it could cut rates three times this year.

Our analysts have confirmed that they will also be a lot less confident if we don’t see a downshift in the BoE inflation forecast and softening guidance at its May meeting to lay the groundwork for a subsequent cut the following month.

Investment markets are remarkably buoyant

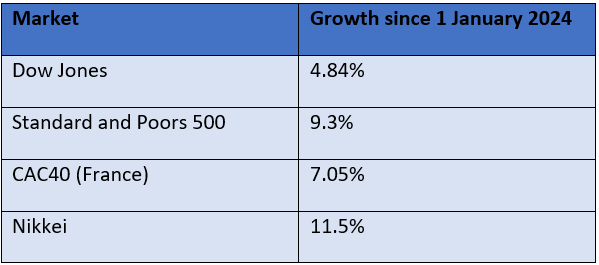

As we head towards the end of the first quarter, possibly the biggest financial story of the year so far is the extraordinary growth in equity values across nearly all developed markets.

For example, you need to remind yourself that all the figures in the table below are year-to-date as at 21 March 2024, and not annualised as you might at first assume!

Source: Kvika Securities

While the FTSE 100 has been far more sluggish so far this year, Morningstar reported that it rose 1.9% on 21 March to its highest level in nearly 11 months at the real prospect of interest rate cuts.

What this means for commercial lending

Clearly, positive news is on the way, with the Times echoing others suggesting rates will start to fall this summer.

Clients looking to refinance once rates do start coming down may be able to do so sooner than they had originally perhaps planned or assumed.

Furthermore, an attractive combination of lower interest rates and low inflation suggest there’s a better environment for investment to drive growth. Indeed, Property Reporter are predicting UK commercial property lending will see a 32% rise in the next five years.

However, a note of caution has to be that rates are unlikely to fall much below “new normal” that Deloittes suggest could be around 3%. They also believe that the days of ultra-low interest rates are now in the past.

In our experience, the commercial property market is adjusting to this higher-rate environment.

Get in touch

We have a wealth of experience when it comes to commercial lending for your clients, even in the most challenging economic circumstances.

To find out more, speak to the Relationship Director in your local office.

Contact Our team today

Richard King

rking@ortussecuredfinance.co.uk

07388 993985

Jamie Russell

jamie@ortussecuredfinance.co.uk

07741 196308